The UK beer industry is evolving, shaped by changing consumer preferences and evolving market dynamics.

Among the most significant trends is the rise of the low and no alcohol category. Its growth in recent years is a response to an evolving societal trend towards wellness and moderation, and subsequent increasing consumer demand for these products.

Brands like Guinness and Clean Co have led the charge, offering alcohol-free versions of traditional favourites that appeal to both health-conscious consumers and those opting for a more mindful approach to drinking.

Leveraging Brand Nudge market intelligence we examined the proliferation of range and also the pricing dynamics for the non-alcoholic beer category across the traditional 'Big 4’ to uncover how this category is evolving.

How has the beer category evolved in the UKs 'Big 4'

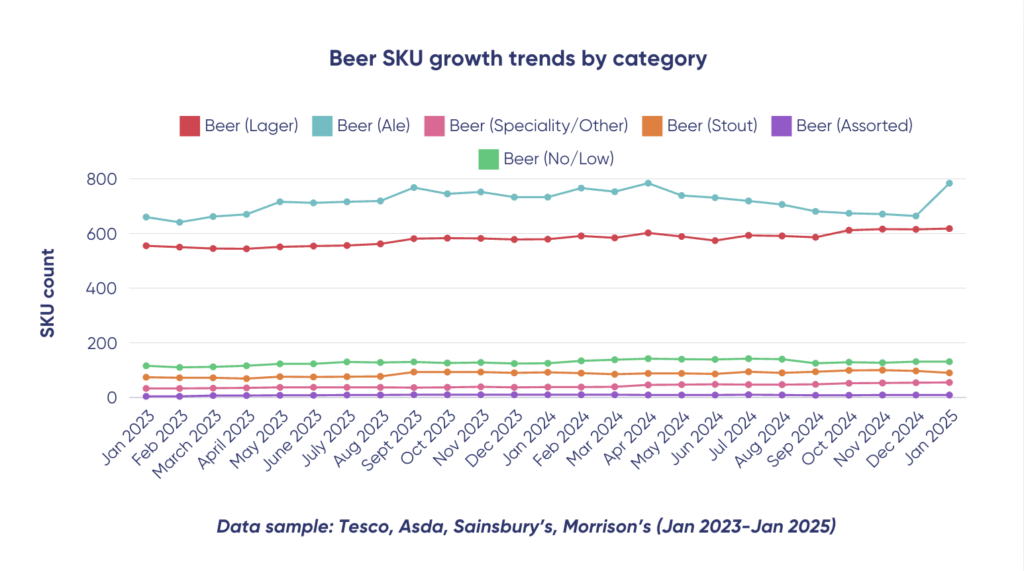

Traditional beer categories such as lager and ale continue to dominate shelf space.

Ale SKU growth: The number of ale SKUs saw a considerable uptick last month (January 2025), rising from 664 in December 2024 to 784 (+120 SKUs).

The number of Ale SKUs has increased by 6.9% YoY (January 2024 vs January 2025).

Lager SKU growth: The number of lager SKUs last month (January 2025) remains similar to the number seen across retailers throughout December, an increase from 615 SKUs to 618 SKUs.

The number of lager SKUs has increased by 6.7% YoY (January 2024 vs January 2025) - at a rate similar to the Ale category, however SKU count remains consistently lower.

Meanwhile, the low and no alcohol beer category, while still smaller, is increasing its presence across the shelves of the ‘Big 4’.

According to The Drinks Business, the UK low and no market more than doubled in 2024 compared to 2023.

Across the ‘Big 4’ retailers, low and no alcohol SKUs increased from 116 in January 2023 to 131 in January 2025 (+12%).

This is a sizable increase in total SKUs and reflects sustained investment in the category by manufacturers and retailers.

Key trends in low and no SKU availability (2023-2025)

Steady growth: The SKU count grew consistently across 2023 and 2024.

Seasonal peaks: SKU counts peaked during summer months (July–August), aligning with increased beer consumption, and dipped slightly in November as retailers made space for seasonal products.

Late 2024 adjustments: A slight decline in late 2024 may indicate market adjustments or streamlined offerings.

Despite fluctuations, the overall trend highlights growing retailer interest in the category. According to the International Wine and Spirits Record (IWSR) volumes in the no-alcohol market are projected to grow at a CAGR of +7% between 2024 and 2028.

While alcohol-free beer now accounts for over 2% of total beverage alcohol sales in the UK, traditional beer remains dominant.

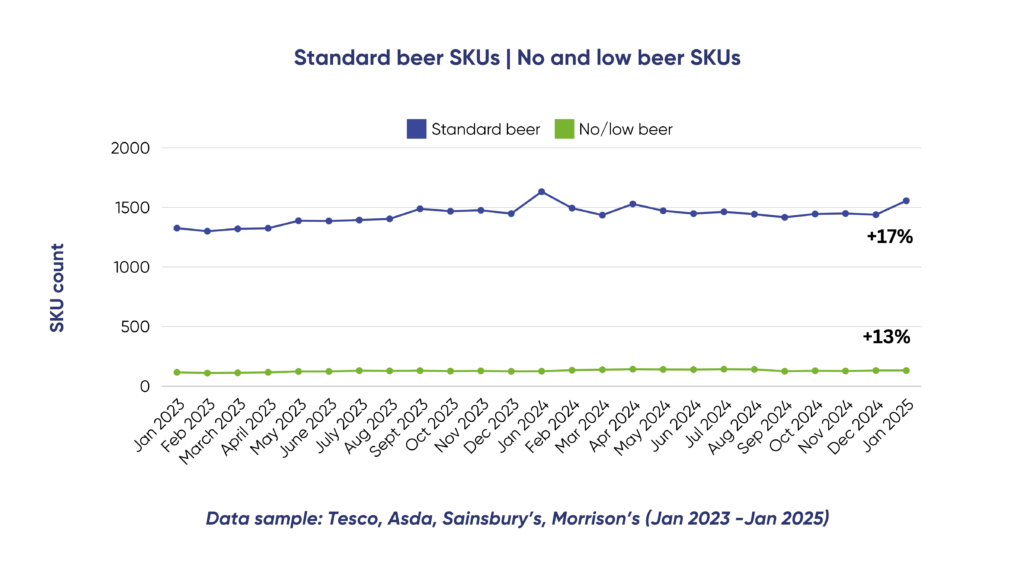

January 2025 SKU snapshot:

SKU growth (2023–2025):

Standard beer (+17%): Standard beer SKU counts increased by 17%, reflecting ongoing innovation and expanded product lines.

Low and no alcohol (+13%): The low and no category grew at a slightly slower rate of 13%, but this growth underscores the rising consumer demand for health-conscious options.

Market implications:

Scale difference: Standard beer still dominates in terms of total SKUs, reflecting its broader consumer appeal and deeper retail penetration.

Continued investment in low and no: The +13% SKU growth signals a shift toward health-conscious consumption but highlights the challenge of competing against the extensive presence of traditional beer.

Retail competition: Securing and maintaining shelf space for low and no alcohol products will become increasingly competitive as brands vie for visibility in this growing segment.

It will be interesting to see how availability for no and low beer continues to evolve throughout 2025, and what new products will emerge from brands investing in the innovation of healthier product lines.

????Top tip: Proactively monitor NPD across retailers and identify which products are gaining or losing shelf space so that you have the intel needed to negotiate better retail placements.

What’s driving the performance of the low and no beer category?

Profitability advantage: For manufacturers, there is a compelling financial incentive. For a standard bottle of alcoholic lager, about 30% of the total cost goes straight to the government in duty.

With non-alcoholic beer, however, skus command a similar RRP to their alcoholic cousins yet manufacturers get to pocket additional margin. This creates a unique opportunity for brands to maintain strong profitability while capitalising on growing consumer demand.

Shifting consumer preferences: Increasing numbers of consumers are prioritising health and wellness, seeking lower-calorie and lower-alcohol options to align with healthier lifestyles. The "Sober Curious" movement, which encourages people to reassess their relationship with alcohol, has also gained traction, particularly among younger generations.

While the no and low alcohol category is especially popular among Gen X and Boomer consumers, Gen Z is emerging as a unique driver of this trend. According to a recent BBC article, many Gen Zers are embracing a ‘sober curious’ lifestyle, driven by a focus on mental health, career ambitions, and mindful living.

Social hurdles remain: That said, societal pressures continue to pose challenges. Research indicates that a third of UK consumers report discomfort with ordering alcohol-free products in social settings, highlighting the need for brands to normalise and destigmatise the consumption of no and low alcohol options.

Guinness vs Heineken: How pricing strategies drive growth in the low and no category

Pricing plays a critical role in category growth.

According to NIQ data for the 52 weeks ending 13 July 2024, Guinness 0.0's off-trade sales surged nearly 110%, reaching £33.2 million.

This impressive growth allowed Guinness 0.0 to overtake Heineken 0.0, becoming the UK's largest alcohol-free beer in the retail sector.

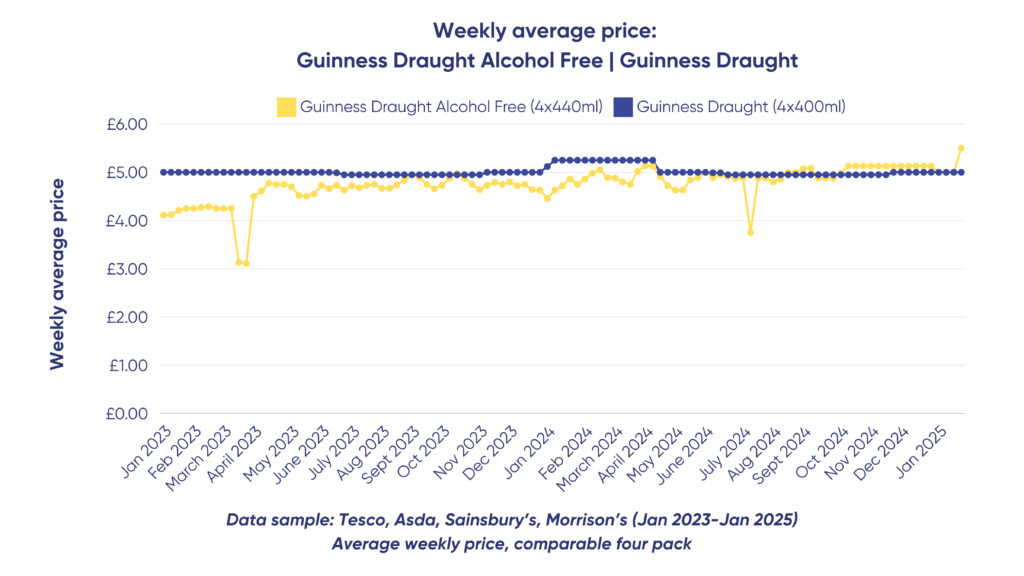

We compared the weekly average price of Guinness 0.0 (4x440ml) and Guinness Draught (4x440ml) across the ‘Big 4’ to understand how it's priced across retailers.

Standard Guinness YoY price change: The average weekly price across retailers has decreased by -2% (January 2024 vs January 2025).

Guinness 0.0% YoY price change: The average weekly price across retailers increased by +23% (January 2024 vs January 2025)

Price stability for regular Guinness: The price of regular Guinness remains fairly stable throughout the two year period, hovering around £5.00.

Price volatility for 0.0% Guinness: The price of alcohol-free Guinness fluctuates more significantly than standard Guinness Draught.

There is a sharp drop in price in April 2023, where it falls significantly below its average.

September 2024 marked the first extended period of time that Guinness 0.0% has been priced higher than standard 4x440ml Guinness Draught.

Convergence of prices: Over time, the price difference between the two products has narrowed, notably in 2024, when both products overlap at around ~£5.

This could indicate a strategic shift toward price parity between alcohol-free and regular options by maintaining the price of its standard SKU and aggressively increasing the price of its 0.0% pack inline with demand.

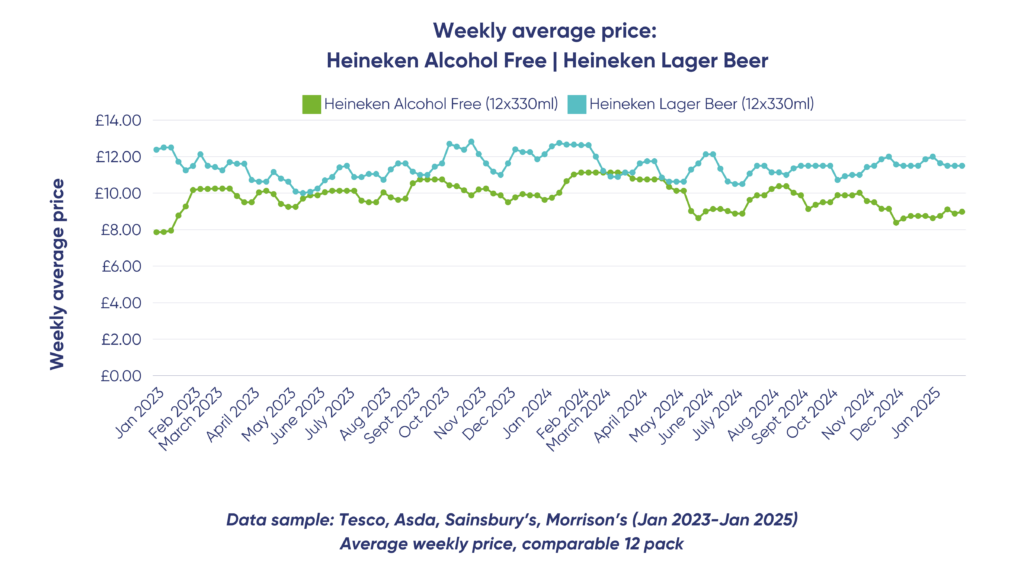

For comparison, we then analysed the average price of Heineken 0.0 (12x330ml) and standard Heineken Lager (12x330ml).

Given Heineken was, up until recently, the UKs leading low and no brand (overtaken by Guinness), it’s interesting to see how differently their SKUs are priced in retailers.

Standard Heineken YoY price change: The average weekly price has decreased by ~3% YoY (January 2024 vs January 2025).

Heineken 0.0% YoY price change: The average weekly price has decreased by -9% YoY (January 2024 vs January 2025).

Consistent price gap: Regular Heineken is consistently priced higher than Heineken alcohol free throughout the two year period, indicating a clear differentiation in pricing strategy.

Price trends: The price of regular Heineken fluctuates notably. Despite fluctuations, regular Heineken’s price remained above £10.00 for most of the period.

Throughout the two year period there remains a considerable delta between the price of its 0.0% 12x330ml SKU and its standard 12x330ml pack.

This month (January 2025) there was a 28% difference in price.

Difference in pricing strategies

There’s a considerable difference in how Guinness and Heineken’s low and no SKUs are priced across the ‘Big 4’.

Whilst Guinness 0.0% increases in price steadily over a two year period, Heineken 0.0 consistently sits at a much lower price point than its alcoholic counterpart.

Interestingly, almost every 0.0% larger SKU listed in the ‘Big 4’ is priced considerably lower than its standard alcoholic SKU - likely having to keep prices low in order to compete against the raft of other options.

Diageo, however, may not face this challenge with Guinness 0.0%, thanks to its strong brand equity and the lack of direct alternatives.

Evolution of low and no beer category pricing

In 2024, UK grocery inflation increased to 1.8%, marking the first rise after 17 months of decline.

Rising inflation often makes consumers more price-sensitive, especially in non-essential categories like alcohol.

This shift leads to cautious spending, with many opting for cheaper alternatives or reducing overall beer consumption.

For low and no alcohol brands, this creates a unique challenge: balancing higher production costs with increasing consumer price sensitivity.

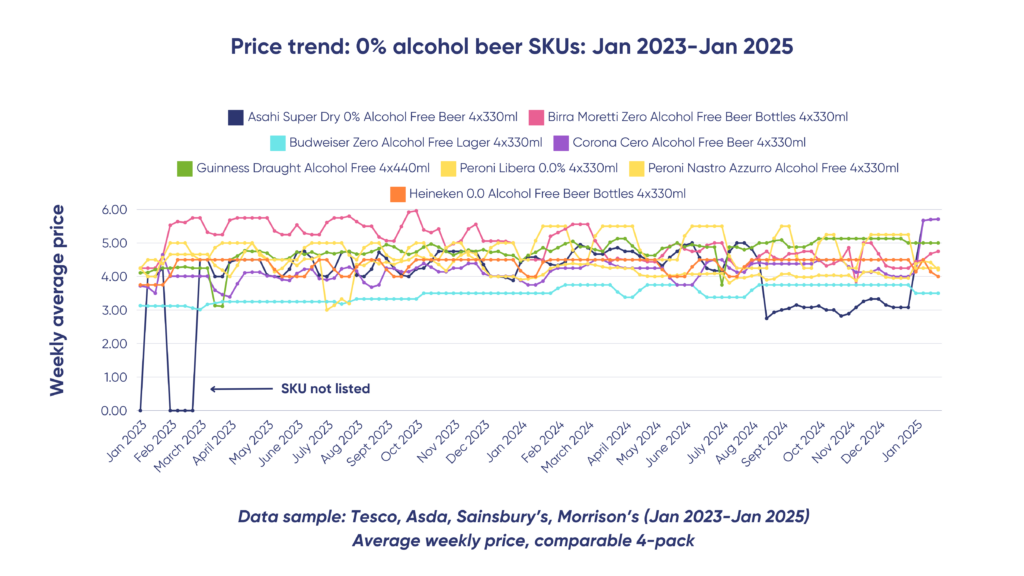

Low and no market price trends

The price trend chart below highlights weekly average price fluctuations for various 0% alcohol beer SKUs between January 2023 and January 2025.

2023–2024: Most brands experienced gradual price increases, with some like Budweiser Zero and Heineken 0.0 maintaining steady prices to stay competitive.

2025 (Jan): A significant price jump for Asahi Super Dry and Corona Cero, while others like Peroni Libera and Birra Moretti Zero saw slight adjustments or drops.

Between January 2023 and January 2025 there has been a general upward movement in prices across several brands.

There could be multiple reasons for this, either to capitalise on the increasing popularity of the low and no category, or in a bid to maintain margins because of increased costs.

What’s next for the low and no beer category?

The low and no-alcohol beer category continues to grow, fueled by health-conscious lifestyles and evolving consumer preferences.

IWSR’s projection that volumes in the no-alcohol market are set to grow at a CAGR of +7% between 2024 and 2025 emphasises the size of the prize for this category, and highlights why manufacturers should be invested in order to capitalise on its long-term market potential.

While product innovation drives growth, strong pricing strategies are equally critical.

Retailers and brands face the challenge of balancing profitability with consumer needs.

By leveraging real-time data and insights, brands can:

To explore how pricing intelligence can help you stay ahead, book a demo with our team. Trusted by over 500 brands, our platform delivers the retail insights needed for fast, strategic decisions.